You filed for bankruptcy. You got the fresh start you needed. Now you are applying for jobs and wondering if that chapter of your financial life is about to walk into the room with you.

Will the employer see it? Which check reveals it? Is there anything you can do?

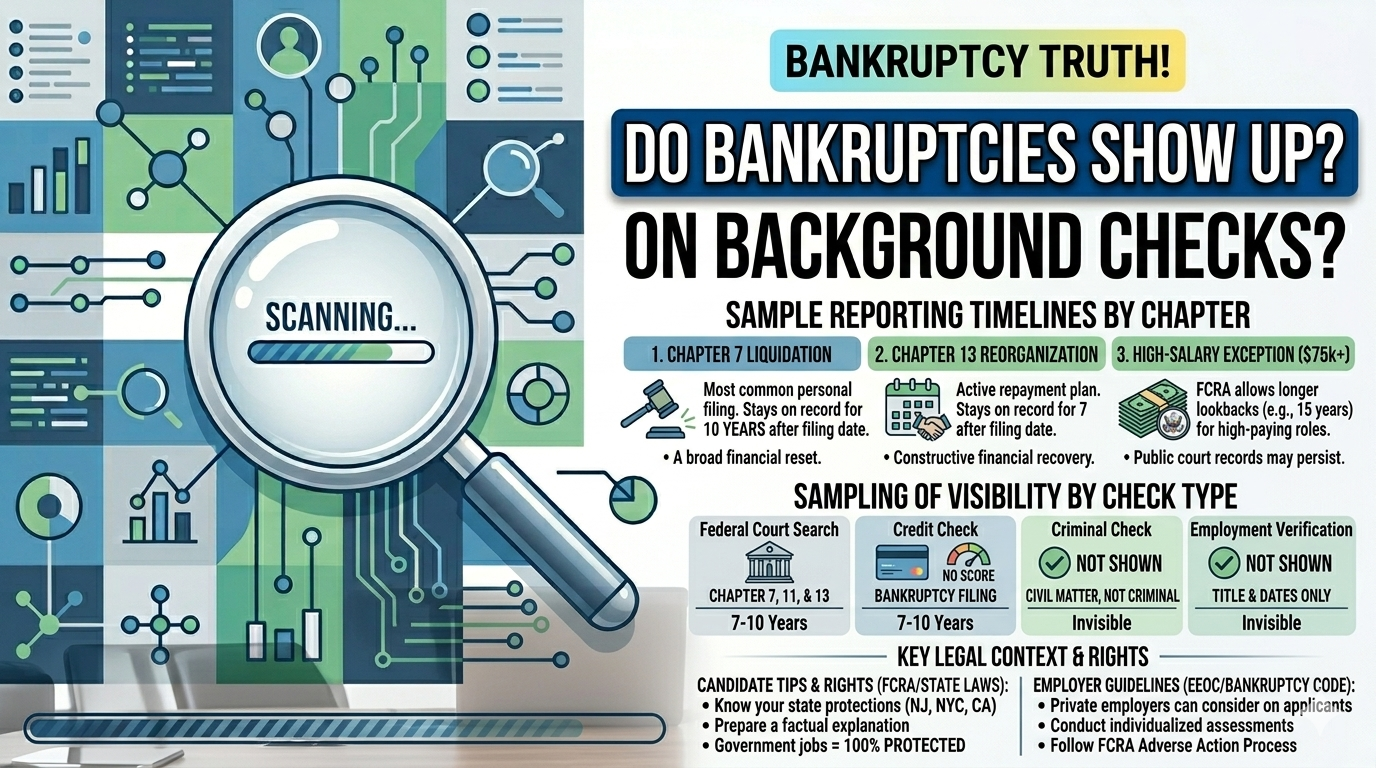

Here is the direct answer: yes, bankruptcies can show up on background checks, but only on specific types of checks. If an employer only runs a criminal background check or an employment verification, your bankruptcy will not appear. If they run a credit check or a federal bankruptcy search, it will. Understanding which check reveals what, and for how long, is the most important thing you can do to prepare.

This guide covers every angle. Which check types surface bankruptcy, how long each chapter stays on record, what the law actually says about employer use of this information, which industries care most, and exactly how to handle it as a candidate.

Quick answer: Bankruptcy appears on credit checks and federal bankruptcy searches, not on criminal background checks or employment verification checks. Chapter 7 stays on record for 10 years. Chapter 13 stays for 7 years. Government employers cannot discriminate based on bankruptcy. Private employers generally can.

Not all background checks are the same package. Employers choose different combinations depending on the role, the industry, and what they are looking for. Here is exactly how each check type handles bankruptcy:

Federal Bankruptcy Court Search

This is the most direct and reliable method for surfacing a bankruptcy. Federal bankruptcy searches pull records directly from the U.S. Bankruptcy Court system. According to iprospectcheck, federal bankruptcy court searches will reveal Chapter 7, Chapter 11, and Chapter 13 filings going back 7 to 10 years. The search returns the filing date, chapter type, case number, and case status.

Not every employer orders a federal bankruptcy search. It is most common for positions involving significant financial responsibility, executive roles, and security clearance requirements.

Credit Check

Credit checks are the most common way a bankruptcy surfaces in a hiring context. When an employer runs a credit check, they receive a consumer report from one of the three major credit bureaus, which includes any bankruptcy filings within the reporting window. According to Checkr, Chapter 7 bankruptcies can stay on a credit report for up to 10 years after filing, while Chapter 13 bankruptcies typically stay for up to 7 years.

A critical nuance: employment credit checks do not include credit scores. Employers see the account history, payment patterns, and major derogatory events like bankruptcies, but not the numeric score.

Criminal Background Check

A bankruptcy will never appear on a criminal background check. This is one of the most important things to understand. As ScoutLogic explains, bankruptcy is a civil matter handled in specialized federal courts. It is not a crime. Criminal checks pull courthouse records for arrests, pending cases, and misdemeanor or felony convictions, none of which have anything to do with bankruptcy.

If an employer only runs a criminal background check, your bankruptcy history is completely invisible to them.

Civil Court Background Check

Standard civil court background checks search local and county civil courts for lawsuits, judgments, estate disputes, and similar non-criminal matters. Bankruptcy filings do not appear in these checks either. As iprospectcheck notes, bankruptcies are handled in specialized federal bankruptcy courts, which are a separate system from the local and county civil courts that standard civil checks search.

Employment and Education Verification

Employment verification confirms your job history, titles, and employment dates with past employers. It contains zero financial information. Education verification confirms degrees and enrollment dates. Neither check will surface a bankruptcy filing under any circumstances.

Security Clearance Investigations

Federal security clearances are the exception that changes everything. A full security clearance investigation includes a comprehensive review of all financial history, including bankruptcy filings, tax liens, significant debts, and financial stress patterns. For government and defense contractor roles requiring clearance, a bankruptcy is reviewed in depth regardless of when it was filed.

Bottom line on check types: Bankruptcy only appears on credit checks and federal bankruptcy searches. If no credit component is included in a background check package, the bankruptcy stays hidden. Knowing what package an employer runs is the first thing a candidate should try to find out.

.png)

Not all bankruptcies are the same, and the type of bankruptcy you filed affects how long it stays on your record and how employers interpret it.

Chapter 7: Liquidation

Chapter 7 is the most common form of personal bankruptcy, representing around 70% of all personal filings according to GoodHire. In a Chapter 7 filing, non-exempt assets are liquidated to pay creditors, and remaining eligible debts are discharged. The debtor must pass a means test showing their income is insufficient to repay debts.

Chapter 7 stays on a credit report for up to 10 years after the filing date. It is the most visible type of bankruptcy from an employer's perspective precisely because it remains on record for the longest period.

Chapter 13: Reorganization and Repayment

Chapter 13 is a reorganization bankruptcy where the debtor keeps their assets but repays creditors through a court-approved plan over 3 to 5 years. It is most commonly used by individuals who have regular income and want to protect their home or other significant property from liquidation.

Chapter 13 stays on a credit report for up to 7 years after filing. Because the debtor is actively repaying creditors rather than discharging all debt, some employers and lenders view Chapter 13 more favorably than Chapter 7. SRA Screening notes that the shorter reporting window reflects the more constructive nature of this filing type.

One practical note: if a Chapter 13 plan requires automatic payroll deductions for repayment, your current employer may become aware of the filing through payroll or HR processes even without running a background check.

Chapter 11: Business Reorganization

Chapter 11 is primarily used by businesses to restructure debt while continuing operations. Individuals with very high debt loads exceeding the Chapter 13 limits may also file Chapter 11. It stays on a credit report for up to 10 years, the same as Chapter 7.

The $75,000 Exception and the Courthouse Problem

Here is the part most guides miss. While FCRA credit reporting limits require bureaus to remove bankruptcies after 7 to 10 years, employment screening companies also pull records directly from federal bankruptcy courts. According to Scherzer.com, under the FCRA's $75,000 salary exception, employment background check companies may report adverse information with no time limit for higher-paying positions. If a bankruptcy exists in public court records, it may still appear on an employment background check even after the credit bureaus have deleted it.

In plain terms: the 7 and 10-year clocks apply to credit bureaus, not to employers who pull courthouse records directly. For high-salary positions, a 15-year-old bankruptcy could theoretically still surface.

The legal landscape here is more nuanced than most people realize, and it creates a significant gap between protections for current employees versus job applicants.

11 U.S.C. § 525(a): Government Employers Are Fully Prohibited

Under Section 525(a) of the Bankruptcy Code, government employers at the federal, state, and local level are explicitly prohibited from denying employment to, terminating the employment of, or discriminating against any person solely because they filed for bankruptcy. This is an absolute prohibition. A public school system cannot refuse to hire a qualified teacher because of a past bankruptcy. A city agency cannot pass over a qualified applicant for the same reason.

The word "solely" matters here. If a government employer has other legitimate reasons to decline a candidate that are separate from the bankruptcy, the law does not prevent them from doing so.

11 U.S.C. § 525(b): The Critical Gap for Private Employers

Section 525(b) covers private employers, and here is where the law becomes significantly less protective. The statute says private employers cannot "terminate the employment of, or discriminate with respect to employment against" individuals who have filed bankruptcy. But notice what that language does not say. It does not say private employers cannot deny employment to applicants.

This gap has been litigated extensively. In the landmark 2011 case Myers v. TooJay's Management Corp., the Eleventh Circuit held that a private employer could lawfully refuse to hire a job applicant based solely on a prior bankruptcy filing. As the American Bankruptcy Institute noted, the Third and Fifth Circuits have reached similar conclusions. The practical result: private employers in most states can legally decline to hire new applicants based on bankruptcy history, as long as they are not terminating a current employee for the same reason.

This is a real and meaningful legal distinction. Your current job is protected. Your next job application is not, unless state law provides additional coverage.

The FCRA Adverse Action Process Still Applies

Even when a private employer decides not to hire based on financial history revealed in a credit check, they must follow the FCRA adverse action process. This means providing a pre-adverse action notice, giving the candidate a copy of the report, allowing a reasonable window to dispute inaccuracies, and issuing a final adverse action notice if they proceed. Skipping this process is an FCRA violation regardless of whether the underlying hiring decision was lawful.

State and City Protections Worth Knowing

Several states and cities go further than federal law. According to Roemerman Law, New Jersey prohibits discrimination against candidates based on bankruptcy history, offering broader protection than federal law.

New York City's Stop Credit Discrimination in Employment Act, part of the NYC Human Rights Law, bars most employers in the city from running credit checks at all, not just from acting on the results. The law covers employers with four or more employees and applies to hiring, firing, promotions, and compensation decisions.

California limits credit checks to specific job types: managerial roles, positions involving regular access to financial accounts, law enforcement, and roles requiring a security clearance. For most other positions, California employers cannot run a credit check under the California Investigative Consumer Reporting Agencies Act. Several other states including Colorado, Connecticut, Hawaii, Illinois, Maryland, Nevada, Oregon, Vermont, and Washington have similar credit check restrictions for employment. Always check local law for your specific state and city.

The weight a bankruptcy carries depends heavily on the industry, the specific role, and what financial responsibilities the position involves.

Finance and Banking

Financial services is where bankruptcy creates the greatest friction. Banks, investment firms, insurance companies, and accounting firms routinely run credit checks as standard practice. Federal regulations, including oversight from bodies like the FDIC, create additional compliance layers. For roles involving direct handling of funds, fiduciary responsibilities, or access to sensitive financial accounts, a recent bankruptcy raises legitimate professional concerns for these employers.

This does not mean automatic disqualification. Many financial professionals have rebuilt their careers after bankruptcy. But the conversation will happen and it needs to be handled well.

Government and Security Clearances

For roles requiring security clearances, financial history is one of the most scrutinized areas of the entire investigation process. The Defense Counterintelligence and Security Agency's adjudicative guidelines treat financial issues as a serious concern because financial stress can create vulnerability to coercion. A bankruptcy does not automatically disqualify someone from clearance, but it requires a thorough explanation and evidence of financial recovery. Cleared employees who file for Chapter 13 after receiving their clearance face the additional complication of potential payroll deductions that can alert HR or management. Despite this, 11 U.S.C. § 525(a) protects government employees from being terminated solely for filing.

Executive and C-Suite Roles

Board-level fiduciary duty and corporate governance concerns mean that executive candidates almost always face credit checks as part of comprehensive background packages. A personal bankruptcy in the background of someone being hired as CFO, COO, or CEO of a company requires context and explanation. The story of how the bankruptcy happened and what financial discipline looks like since then matters enormously in these conversations.

Healthcare

Clinical roles in healthcare rarely trigger credit checks. However, financial or administrative roles within healthcare systems, particularly those involving billing, procurement, or fund management, may include a credit component. State licensing boards have independent authority and may consider bankruptcy in licensing decisions depending on the profession and jurisdiction.

Technology and SaaS

Most technology companies run standard background packages focused on criminal history, identity verification, and employment verification. Credit checks are uncommon unless the role involves handling customer financial data, financial operations, or executive responsibilities. A software engineer, product manager, or designer at a tech company is unlikely to face a credit check as part of their background screening.

The worst approach is to hope it does not come up. The second worst is to be caught flat-footed if it does. Here is a practical framework.

Find Out What Checks Are Being Run

Employers are required to notify candidates in writing before running a credit check and must obtain consent. When you receive a background check authorization form, read it carefully. If it includes a credit check or civil/financial records component, prepare accordingly. You can also ask HR directly what types of checks are included in their screening package.

Pull Your Own Credit Report First

Before the employer sees your credit report, see it yourself. You are entitled to free annual credit reports from all three major bureaus at AnnualCreditReport.com. Check that the bankruptcy is accurately reported, falls within the correct timeline, and that no errors exist. If a bankruptcy was discharged more than 10 years ago for Chapter 7 or 7 years ago for Chapter 13, it should no longer appear. If it does, file a dispute with the credit bureau.

Prepare a Concise, Professional Explanation

If the bankruptcy will surface and is relevant to the role, have a clear explanation ready. The best explanations are brief, factual, and forward-looking. What happened, what you learned from it, and what your financial picture looks like today. Employers are not necessarily looking for a perfect record. They are looking for honesty, self-awareness, and evidence that the situation is in the past.

Avoid oversharing, emotional narratives, or placing blame. Two to three sentences is usually enough unless the interviewer asks for more.

Demonstrate Financial Recovery

A bankruptcy that happened eight years ago and is followed by a consistent track record of on-time payments, stable finances, and responsible credit management tells a very different story than a bankruptcy that happened two years ago. If you have rebuilt your credit, have a stable financial picture, and can demonstrate recovery, make that part of the conversation.

Know Your State's Protections

If you are in New Jersey, New York City, California (for most roles), or one of the states with credit check restrictions, your employer may not even be able to run a credit check. Understanding your legal environment before the process starts gives you a significant advantage.

Target Roles Where Credit Is Not Relevant

Strategic targeting reduces your exposure significantly. Roles in technology, education, non-profits, creative industries, and many mid-level positions at large corporations rarely include credit checks. Applying your skills in these directions while rebuilding your financial reputation is a practical strategy rather than a workaround.

Government Roles Offer the Strongest Protection

Because government employers are prohibited by law from denying employment based on bankruptcy, public sector positions represent the most protected category for candidates with bankruptcy history. If you are a strong fit for government roles, the legal protection under Section 525(a) is meaningful and real.

Employers who encounter bankruptcy history on a background check need a consistent, documented process to avoid both discriminatory practices and negligent hiring claims.

Does chapter 7 bankruptcy show up on an employment background check?

It depends on the type of check. Chapter 7 will not appear on a criminal background check or employment verification. It will appear on a credit check or federal bankruptcy search for up to 10 years after the filing date. For positions paying over $75,000, it may appear even beyond that window if courthouse records are searched directly.

Can an employer fire me for filing bankruptcy?

No. Under 11 U.S.C. § 525(b), private employers cannot terminate a current employee solely because they filed for bankruptcy. Government employers face the same prohibition. This protection applies to current employees, though the protections for job applicants at private companies are significantly weaker.

How long does chapter 13 bankruptcy stay on a background check?

Chapter 13 stays on your credit report for up to 7 years after the filing date. Federal bankruptcy court records may be searchable for a similar period through background screening companies, though the FCRA's $75,000 salary exception means higher-paying positions may face searches without a firm time limit.

Will bankruptcy affect my security clearance?

Bankruptcy itself does not automatically disqualify someone from a security clearance, but it triggers a detailed financial review. Investigators look at the circumstances, whether the situation is resolved, and whether there are ongoing financial stressors that could create vulnerability. A single bankruptcy years in the past with a strong financial recovery is treated very differently than ongoing financial distress.

Are there states where employers cannot check my bankruptcy history?

Yes. New York City bars most employers from running credit checks at all. New Jersey prohibits discrimination based on bankruptcy history. California restricts credit checks to specific job categories. Colorado, Connecticut, Hawaii, Illinois, Maryland, Nevada, Oregon, Vermont, and Washington also have credit check restrictions for employment. Government employers in every state are prohibited from discriminating based on bankruptcy under federal law.

What if my bankruptcy is no longer on my credit report but the employer finds it in court records?

Bankruptcy filings are public records in the federal court system. Even after a credit bureau removes the record, a background screening company can pull it directly from courthouse records. Under the FCRA's $75,000 salary exception, this older information can still be reported on employment checks for higher-paying positions. There is no legal mechanism to make public court records disappear.

Should I disclose a bankruptcy before being asked?

In most cases, no. Proactive disclosure is rarely necessary and can introduce a red flag before the employer has reason to look for one. If you are applying for a role that clearly requires a credit check (financial services, executive roles, government positions requiring clearance), having your explanation prepared and being ready to address it professionally is the better approach.

Bankruptcy is not a career-ending event. But it is a piece of your financial history that requires strategic awareness, not wishful thinking.

The key things to remember:

Bankruptcy law exists precisely to give people a fresh start. The law on employment discrimination gives that fresh start some real protection, at least for the roles where it matters most. Know the rules, know your rights, and show up prepared.

Sources

Checkr: Bankruptcy Background Check Guide

iprospectcheck: Do Bankruptcies Show Up on Background Checks

GoodHire: Bankruptcy Background Checks Complete Guide

SRA Screening: Do Bankruptcies Show Up on Background Checks

ScoutLogic: Do Bankruptcies Show Up on Background Checks

Scherzer: Bankruptcy Records and Employment Background Checks

Legal Information Institute: 11 U.S.C. § 525

American Bankruptcy Institute: Discrimination in Hiring

Roemerman Law: Bankruptcy and Employment Discrimination

Furr Cohen: Private Employers and Bankruptcy Discrimination